War

Cycles

Previously I have shown that the Strauss

and Howe saeculum is aligned with Kondratiev price

cycles

before 1650. The Kondratiev cycle at this time was shown to be consistent with

a lagged Malthusian

population growth model. Table 1 presents these Kondratiev cycles in terms

of its half-cycle or Kondratiev wave. Kondratiev waves are typically defined as

alternating periods of high and low inflation rate, but in this case they are

periods of alternating high and low price level. This is because the Malthusian

model predicts alternating periods of feast and famine that should be associated

with low and high price levels, respectively. In all but one case the expected

correspondence between the theoretical cycle driver and price level was seen. Also

shown in the figure is socioeconomic stress, defined as the frequency of social

unrest divided by the frequency of construction starts for religious buildings.

The former is a measure of social turmoil while the latter is an economic

indicator (presumably, famine period should be associated with both high price

level and low rate of construction starts, giving a large ratio between the two

(high socioeconomic stress). Feast periods would show the reverse, a small

ratio and low socioeconomic stress. With two exceptions, periods of feast or

famine correlated with low or high socioeconomic stress, respectively.

Table 1. Pre-1650 long

cycles showing the action of the Malthusian population model (data from Table 1

in population model)

|

Turning |

Kondratiev wave |

Driver |

Price |

Socioeconomic stress |

|

-- |

1176-1202 |

Feast |

Low |

Low |

|

-- |

1203-1230 |

Famine |

High |

High |

|

-- |

1231-1254 |

Feast |

Low |

Low |

|

-- |

1255-1282 |

Famine |

High |

Low |

|

-- |

1283-1305 |

Feast |

Low |

High |

|

-- |

1308-1328 |

Famine |

High |

High |

|

-- |

1329-1352 |

Feast |

Low |

Low |

|

-- |

1353-1381 |

Famine |

High |

High |

|

-- |

1382-1405 |

Feast |

Low |

Low |

|

-- |

1406-1435 |

Famine |

High |

High |

|

1435-1459 |

1436-1459 |

Feast |

High |

Low |

|

1460-1487 |

1460-1487 |

Famine |

High |

High |

|

1488-1517 |

1488-1520 |

Feast |

Low |

Low |

|

1518-1542 |

1521-1557 |

Famine |

High |

High |

|

1543-1569 |

1558-1579 |

Feast |

Low |

Low |

|

1570-1594 |

1580-1602 |

Famine |

High |

High |

|

1595-1621 |

1603-1626 |

Feast |

Low |

Low |

|

1622-1649 |

1627-1650 |

Famine |

High |

High |

A

long cycle in Anglo-American history which I call the PE cycle has been

approximately aligned with the Straus and Howe saeculum since 1720. The paradigm model was developed

to explain both cycles for the period since ca. 1820. This paper attempts to

address the period between 1650 and 1820 that is not covered by either model.

The PE cycle was defined as a consensus

between the Schlesinger political cycle and an economic cycle based on dates

for financial crises. The political cycle begins with the American revolution, and the first financial crisis which had an

impact on American politics was in 1772. Between 1774 and 1860 the PE cycle

periods were fairly well aligned with Kondratiev waves, as were the

corresponding Strauss and Howe turnings. The alignment between turnings and

Kondratiev waves continued further back and the PE cycle was extended before

1774 to 1720 using the consensus dates from Goldstein1 for these

waves. Before 1720 the alignment ends and the PE cycle is considered to have

begun them.

Table 2 adds the 1650 peak and 1689

trough (dating from Goldstein1) to give a set of eight periods

between 1650 and 1860 that correspond to Kondratiev waves, exactly before 1774

and approximately afterward. These periods were analyzed in terms of inflation

rate, unrest frequency and war intensity. Statistically significant relations

were seen with all three: upwaves are times of inflation, increased war and

lower unrest; downwaves are the opposite. That is unrest was inversely correlated

with price: high prices/inflation were good times with low levels of unrest.

Before 1650 unrest was directly correlated with price: high prices/inflation were bad times with high levels of unrest. This shift in

social and economic interactions implies that a new cycle mechanism had come

into play after 1650.

Table 2. Socioeconomic

dynamics of long cycles over 1650-1860

|

Turning* |

PE period |

Description |

Unrest events |

Inflation rate |

War Deaths per 100K pop. |

|

1649-1675 |

1651-1688 (A) |

Recession |

0.98 |

-0.8% |

25.3 |

|

1675-1704 |

1689-1719 (I) |

Prosperity |

0.58 |

0.9% |

71.9 |

|

1704-1727 |

|||||

|

1727-1746 |

1720-1746 (A) |

Recession |

1.38 |

0.2% |

16.1 |

|

1746-1773 |

1747-1774 (I) |

Prosperity |

0.79 |

1.0% |

43.8 |

|

1773-1794 |

1774-1792 (A) |

Recession |

1.00 |

1.0% |

11.0 |

|

1794-1822 |

1793-1823 (I) |

Prosperity |

0.45 |

0.8% |

66.3 |

|

1822-1844 |

1824-1842 (A) |

Recession |

1.96 |

-1.1% |

2.2 |

|

1844-1860 |

1843-1859 (I) |

Prosperity |

0.43 |

1.5% |

11.3 |

|

Average (n=4) |

|

|

-0.16% |

48.3 |

|

|

Average 1650 (n=4) |

|

1.33 |

1.05% |

13.7 |

|

|

|

p <= |

|

3.8% |

3.7% |

4.0% |

*Social moment turnings (crises and awakenings) in bold

Numerous observers, including Kondratiev,

noted an association between upwaves and concentrations of war. Figure 1 shows a plot of

war intensity, defined as deaths in great power2 wars per 100,000 population.1 War intensity shows 50-year

cycles from the late 16th through early 20th centuries

(see Figure 1).

Concentrations of war do tend to occur during upwaves, which is reflected in

the average war intensities in Table 2. These concentrations of war can be characterized

in terms of the largest war within it, which is called a peak war. This

terminology reflects a rough correspondence between the peak wars and

Kondratiev peaks. The peak wars relevant to America are the War of Spanish

Secession (Queen Annes war),

Seven Years War (French & Indian war), the War of 1812, the American Civil

War and World War I.

Figure 2 shows a plot of

British imports3 relative to their long term trend over the 18th

century. Since colonial America was a key supplier of these imports, this data

can give some insight into economic trends in the colonies. Also shown is a

plot of US real unskilled labor costs4 for the 1790-1860 period. Figure 2 shows downturns

in trade over 1724-46 and 1775-1790 and a period of zero wage growth over 1824-46.

Figure 3 shows a

continuation of the labor cost trend over 1850-1940. Real per capita GDP5

relative to its long trend is also plotted as a second economic indicator. The

period is broken into four eras: 1846-1893 when wages were rising and GDP

growth was above trend; 1893-1915 when wages were flat and growth was below

trend; 1915-1929 when wages were rising and growth was on trend; and 1929-1940,

which corresponds to the Great Depression. Two of these eras, 1893-1915 and

1929-1940 define periods of long-term economic decline. These two eras roughly

correspond to periods of rising/elevated unrest (Figure 3). Table 3 presents

these five periods of economic decline along with the end of the preceding peak

war. Shortly after the end of the peak war and before the start of the downturn

were the beginnings of war debt reduction (austerity). Dates for this are given

in Table 3. Finally, dates for major financial crises associated with turning

points in the PE cycle are given.

Table 3. Clustering of cycle turning points, peak wars, peak debt, panic and

depression.

|

Peak War |

War end |

Start of

austerity |

Downturn |

Financial

crisis |

Consensus turning point |

PE active

period |

Social moment

turning |

|

War

of Spanish Secession |

1713 |

1717 |

1724-1746 |

1720 |

1721 |

1720-1847 |

1727-1846 |

|

Seven

Years War |

1763 |

1765 |

1775-1790 |

1772 |

1771 |

1774-1892 |

1773-1894 |

|

War

of 1812 |

1814 |

1819 |

1824-1846 |

1819 |

1821 |

1824-1842 |

1822-1844 |

|

Civil

War |

1865 |

1870 |

None |

1873 |

1869 |

1860-1873 |

1860-1865 |

|

None |

-- |

-- |

1893-1915 |

1893 |

1892 |

1896-1919 |

1886-1908 |

|

World

War I |

1918 |

1922 |

1929-1940 |

1929 |

1927 |

1930-1946 |

1929-1946 |

The

sequence of events in four of the six entries in Table 3 are

consistent with the following model. Fighting wars results in

a substantial increase in government outlays, which acts as an economic

stimulus, increasing economic output and the price level. Hence periods

when wars are fought should show inflationary prosperity, which is reflected in

low levels of unrest and inactive periods in the PE cycle. Spending for wars

leads to growth in government debt. At some point after the wars have ended,

the government will begin to pay down its war debt by running budget surpluses

(austerity). Imposition of austerity produces a disinflationary economy prone

to financial crisis and prolonged economic downturns. Eventually both happen,

triggering rising unrest and the beginning of an active period in the PE cycle.

This sequence of events typically takes about a decade. I call this mechanism

the war model.

The

model breaks down for the Civil war. The expected sequence of end of the peak

war, start of austerity, and financial crisis occurred, but the downturn did not

materialize. Although the Panic of 1873 triggered the longest recession in

American history, it was followed by a very strong recovery. The entire postwar

era saw a rising trend in real wages (Figure 3). Not

surprisingly there was no significant rise in unrest for two decades after the

war. The 1860s do correspond to an active period and crisis turning, but both

of these began before the Civil War. In fact it was the war itself, not an

economic downturn, that was the driver for the crisis.

Furthermore, a period of economic downturn beginning with the panic of 1893 and

which showed elevated level of unrest was identified (Table 3). This period also

corresponds to an active era in the PE cycle and an awakening turning, but it

has no peak war. Two successive failures of the war model indicate that

sometime between the War of 1812 and the Civil War, the war mechanism was

replaced by another. This new mechanism was the paradigm mechanism previously described.

Historical

action of war-linked financial crisis in the generation of active periods and

social moments

The

population model was still valid at the 1650 Kondratiev peak, but by the next

peak in 1720 the war model was applicable. The unusually long Kondratiev cycle

between these two dates contained three turnings instead of the normal two: an unraveling

turning over 1649-75, the Glorious Revolution Crisis over 1675-1704 and a high turning

over 1704-1727. Key reforms enacted as a result of the Glorious Revolution were

responsible for the appearance of the war mechanism.

The

direct result of the revolution in 1688 was the installment of a new king, William

III, who recognized Parliament as a co-equal partner with the monarchy. When

William proposed war with France, Parliament duly declared war in May 1689. The

Commons, which had been responsible for authorizing war supply since the 15th

century, deliberately kept William underfunded, requiring frequent war spending

authorizations by Parliament, which kept Parliament in session almost

continuously.6

Parliament

developed innovative new taxes which were actually paid because they were seen

by the public as legitimate because they came from Parliament. This established

a regular means for securing government income that could be adjusted to actual

needs. Parliament established a Commission of Public Accounts in 1690 to

monitor government expenditures by the Crown and began inserting appropriations

in its revenue bills that directed how the money was to be spent.6

Through

these provisions Parliament gained control over the government budget, which

helped ensure the success of the new central bank created in 1694.6 Not

only was there now public control over government finance, budgetary issues

were now explicit, allowing proper analysis of government debt as an investment.

This created a direct link between government finance and the London financial

and commercial community. In 1698 John Castaing began to issue a list of stock

and commodity prices called The Course of

the Exchange and other things at Jonathans Coffee House. It is the earliest

evidence of organized trading in marketable securities in London.7

These

innovations, collectively called the Financial Revolution, created market mechanisms

through which wars could directly affect financial markets, leading to price

rises (bubbles) and declines (financial crisis). An excellent example of this

is the South Sea bubble. The South Sea Company was formed in 1711 as Tory competitor

for the Whig Bank of England.8 The company was granted a monopoly on

all British trade with the Spanish colonies in South America (then called the

south sea trade) in exchange for taking over and consolidating the national

debt. Consolidation meant getting owners of pre-existing loans to exchange them

for South Sea company stock that paid a dividend that was smaller than the

interest payment on original loan, which saved the government money. Holders of

the loans were willing to do this for two reasons: (1) the stock was a liquid

asset and so carried a liquidity premium, and (2) the stock had a potential for

capital gain that the existing debt did not. What the South Sea company did was

convert government debt from an investment (asset purchased for the income it

provides) into a speculation (assets purchased for their capital gains

potential). This is analogous to the recent practice of converting conventional

mortgage loans into tradable mortgage securities.

The

outcome was similar to what happened three centuries later. After the company

directors circulated false claims of success in the South Sea trade the stock

took off.8 Speculative fires were stocked when the government

endorsed the company proposal for addition debt conversion over that of the

Bank of England.8 The rising price of company stock helped spur

general interest in the stock market as did the internet bubble. By the middle

of 1720 market was flooded with a remarkable range of new ventures (the Pets.com

of their day). Parliament passed the Bubble Act to outlaw the formation of

these companies in an effort to prop up South Seas stock by minimizing

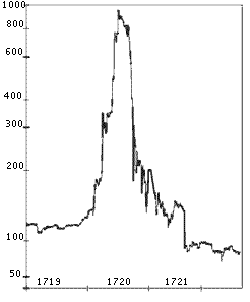

competition for investor money. The stock peaked in early August and collapsed soon

after (Figure 4). It continued

to fall well into the next year, devastating institutions and individuals alike.8

Although historians have often assumed

that this crisis, like later ones, had serious economic consequences, there is

little statistical support for this.9 As

shown in Figure 2, a downturn in

trade volume relative to trend began years after the crisis. It did have

serious political consequences, however, but these did not extend to America. This

is not the case for the next war-linked financial crisis in 1772. Although the

direct impact of the crisis was on the City of London, it exerted indirect

effects that led to the American revolution as described by Schwarz:10

In

the summer and fall of 1772, panic took hold of Londons financial circles. It began with the collapse

of a firm called Neale, James, Fordyce, & Down. Alexander Fordyce had been

speculating successfully for a decade, but in the early 1770s his investments

went sour. He managed to deceive his partners for a while; according to one

biographer, It is said he succeeded in quieting their

fears by the simple expedient of showing them a pile of bank notes which he had

borrowed for the purpose for a few hours. When things got too hot, though,

Fordyce skipped town owing a hundred thousand pounds. In early June his firm

suspended payment of its debts.

In

a generally overextended market many other firms were just as vulnerable, and

the dominoes started falling. By the end of June twenty major houses had

collapsed. Those that were left suffered the usual squeeze: Debtors were slow

to pay, while creditors were quick to demand payment. Among the hardest hit was

the already foundering East India Company, which had a monopoly on trade,

chiefly in tea, with the British Asian colonies.

In

September the company took out a loan from the Bank of England, to be repaid

from the sale of goods later that month. But with buyers scarce, most of the

sale had to be postponed, and when the loan fell due, the company coffers were

empty. On October 29 the bank refused to renew the loan. That decision set in

motion a chain of events that made the American Revolution inevitable.

The

East India Company had eighteen million pounds of tea sitting in British

warehouses. Selling it in a hurry would do wonders for its finances. The

American market beckoned, but there were two problems. First of all, the

company was required by law to sell its tea to the highest bidder in England,

letting merchants there and in America ship and resell it. Second, tea sold in

America carried a tax of three pence a pound, which made it unpopular with restive

colonists.

After

prolonged wrangling, in May 1773 Parliament let the company eliminate the

middleman and market the tea itself through its own American agents. It also

refunded duties that the company had paid upon bringing the tea to England.

With these changes the East India Company could easily undercut the smugglers

who had been taking much of its business. On the tax issue, however, the

government would not budge. While admitting that three pence a pound yielded

negligible revenue, it insisted on maintaining British taxation power over its

colonies.

It

seemed a perfect compromise: The company would make

money, the colonies would get cheap tea, and Britain would uphold its rights.

So the government was quite surprised when citizens in Charleston,

Philadelphia, New York, and most famously Boston vigorously rejected the

tainted tea. Their tea parties showed that America would not be bribed into

accepting taxation without representation. Yet that was not the only issue.

There

was nothing new about the tea tax. Colonists had been paying it--and similar

taxes on sugar, molasses and win--for years. The new and obnoxious feature of

the Tea Act was the monopoly for the East India Company, which would deprive

American merchants of their business in both legal and smuggled tea (and which

they feared would be extended to many other goods). By

alienating this wealthy and powerful group, the British united self-interest

and revolutionary fervor in a combination that would soon destroy the colonial

bond. Just as the failure of a single bank had caused a financial panic, so too

did a seemingly innocuous attempt to collect a tax that was already on the

books lead directly to the American Revolution.

Within

two years of the tea parties, armed rebellion had broken out, which expanded to

full-scale war by the next year. The outbreak in hostilities led to the

downturn in trade that began in 1775. So the crisis of 1772 led to both

political and economic changes consistent with the start of an active period or

social moment turning and can be considered as a triggering event for both.

The

role of the Panic of 1819 in the rise of Jacksonian populism that characterized

the 1824-1842 active period in the PE cycle was previously discussed. This crisis

ended the Era of Good Feelings by accentuating political division over the role

of the central bank in the panic. In time these divisions became formalized in

the establishment of the Democratic and Whig parties, and the rise of the

paradigm mechanism. Here the war-induced financial crisis gave rise not only to

economic stress and its associated unrest, but also to political forces that

produced a liberal era and the paradigm derived from it.

As

described earlier, the next war-linked financial crisis, the Panic of 1873, did

not play a role in initiating a social moment turning or active period for a

crisis turning and active period in the PE cycle. Financial crisis continued to

be a factor in producing active eras/social moment turnings after 1873. In

fact, in three of the four active eras/social moment turnings after the Civil

War, financial crises (in 1893, 1929 & 2008) played important roles. Since

1720, only two of the eight active eras/social moments have not involved

economics as a dominant factor. Both of these (Civil War and Civil rights era)

had triggering events associated with an overriding social issue (race

relations).

The

genesis of the modern politically-driven cycles (war and paradigm) was the

financial revolution associated with the Glorious revolution. Strauss and Howes generational cycle characterizes this period as

secular crisis, a period that addresses the outer world of institutions, as

opposed to the spiritual awakening, which addresses the inner world of private

belief and behavior. Social moments correspond to active eras in the PE cycle,

but the PE cycle methods do not apply to this time, nor do the social dynamics support

a Glorious Revolution social moment, (unrest was not particular high at this

time). This period occurs outside of the scope of my empirical cycle methods,

although it is undeniably a crisis era in the sense that Strauss and Howe use. It

is only after this crisis that the patterns characterizing the PE cycle became

valid.

From the very beginnings of financial

markets in the wake of the Glorious Revolution, finance has been intertwined

with politics, with the latter in the drivers

seat. Initially, it was war policy by the monarch that was the driver. Quincy

Wright, who was first to characterize the war cycle, proposed a number of

factors as possible causes for periodicity of war. One

factor were alternating hawk and dove generations: The warrior does not wish to

fight again himself and prejudices his son against war, but the grandsons are

taught to think of war as romantic.12 The financial impact of these

cyclical wars produces cyclical unrest that defines the PE and turning cycles. With

the rise of mass democracy, I have proposed dominant and recessive paradigmic

generations to replace hawk and dove generations, but it is still the impact of

politics on policy affecting the economy and society that gives rise to active

eras and social moments. For example the recent financial crisis was made

possible by decades of supply side economic policy introduced as part of the

Freedom paradigm established during the 1966-1981 active era. Since then, high

interest rates, as opposed to high taxes, have been the preferred means to

control inflation, which penalizes capital-intensive industries like

manufacturing, to the benefit of finance. Preferential tax treatment of capital

gains over income encourages speculation as opposed to investment, much as did government

sponsorship of the South Sea company.

Development

of the War Cycle

As Figure 1 shows, there is

some evidence for the cycle existing as early as the late 16th century, and certainly during the first half of the 17th

century. Early 16th century wars showed no evidence of cycles (see Figure 5). Interactions

between war finance and the Kondratiev cycle can explain the rise of the war

cycle. Wright proposed that financial constraints force temporary cessations of

war expenditure to give the economy time to recovery: there is a tendency to

postpone a new war until there has been time to recover economically from the last.13

The scale of warfare had grown

tremendously during the 16th and early 17th centuries culminating in the

cataclysm of the Thirty Years War, a phenomenon called the Military revolution.

This growth placed a severe strain on the ability of nations to pay for the

wars they fought. Spain was the only belligerent involved in all these major

wars and for whom the problem of payment was most acute, Despite the steadily

increasing stream of silver and gold from their American colonies, Spain

underwent no less than seven state bankruptcies over the 1500-1650 period.14,15

Most of these bankruptcies came from excessive war-spending. The bankruptcies

of 1557 and 1607 more or less forced the Treaty of Cateau-Cambresis

in 1559 and the truce of 1609 which established the de facto independence of the Netherlands from Spain. Spain never

learned to reign in her ambitions and when the growth in flow of American

treasure slowed in the 1630s, she began a permanent decline that ended her days

as a great power by the end of the century. As the Spanish captains used to

say, victory went to him who has the last escudo.15

The example of Spain could serve as an

object lesson in the problems that came from ignoring finance. The other

European powers had the luxury of not always being involved in conflict, and so

were better able to time their war-fighting so as to avoid fiscal catastrophe. The

population-derived Kondratiev cycle created alternating periods of higher or

lower inflation. The former were good times to incur debt since it could be

repaid using less valuable currency. Hence there was a natural tendency for

wars of choice to cluster during upwaves, giving rise to a war cycle aligned

with the Kondratiev cycle as depicted in Figures 1 and 4. That is, price

cycles of feast/famine(and the associated good/ bad

times) induced cycles of peace/war, which, as the financial revolution

unfolded, induced cycles of depression/prosperity (associated with bad/good

times). That is, around the time of the Glorious revolution, the alignment

between unrest and price shifted from inflation being bad (famine) to inflation

being good (prosperity). Such a shift would necessarily affect the alignment

between Kondratiev cycles and the saeculum. The 1650-1843 period

contains 3.5 Kondratiev cycles of 55 years, implying a saeculum length of 110

years at the normal ratio of two Kondratievs per saeculum. The shift in

alignment caused by the financial revolution forced the addition of one extra

turning in order to avoid sequential social moments. This means that two

saecula fell into the 1650-1843 period containing only 3.5 instead of 4 Kondratievs.

This implies a shortening of the saeculum length from 110 to 96 years. The actual

average saeculum length for the two saecula before 1649 was 107 years, compared

to 94 years for the two after.

Summary

This graphic summarizes the various long

cycles I have described in terms of when they were operative The first four

rows describe an economic cycle, a generational cycle, a political and economic

cycle, and a war cycle. The next two rows show when the three models I have

presented were operational. Overlapping the beginning of each model is the

revolution that made the mechanism possible. The military revolution created

the need for finance, which led to the war cycle. The financial system created

to manage wars during the financial revolution spawned the war cycle, which

after the democratic revolution was replaced by the paradigm mechanism.

|

12th cent |

13th cent |

14th cent |

15th cent. |

16th cent. |

17th cent. |

18th cent |

19th cent |

20th & 21st cent |

|||||||||||||

|

|

50-year Kondratiev cycles |

Long K-cycle |

|||||||||||||||||||

|

|

Century-long saeculum |

Variable length saeculum |

|||||||||||||||||||

|

|

PE cycle |

||||||||||||||||||||

|

|

War Cycle |

|

|||||||||||||||||||

|

|

Malthusian Model |

|

Paradigm model |

||||||||||||||||||

|

|

War model |

|

|||||||||||||||||||

|

Revolutions: |

Military |

Financial |

Democratic |

|

|||||||||||||||||

References

1.

Goldstein,

Joshua S. Long Cycles, New Haven: Yale University

Press, 1988

2.

In 1650 the great powers were the Austrian empire, Britain, France, the

Netherlands, the Ottoman empire, Prussia/Germany,

Spain and Sweden. Sweden, the Netherlands and the Ottomans are dropped after

1715 while Russia is added. Spain drops out after 1800; the United States and

Italy are added after 1850.

3. British import volume is the

official value (in British pounds) of

imports. It was obtained from Mitchell (ref 13) for the period 1700-1853. A

second series of computed values is given for 1796-1853. The ratio of the

computed values to the official value shows a shape similar to the price index

over the 1796-1853 period. If the computed values are

divided by a price index to put them in real terms the resultant series is very

similar to the official series. Thus, the official trade statistics appear to

be a proxy for trade volume in real terms and so were used directly for

analysis.

4.

Lawrence

H. Officer and Samuel H. Williamson, Annual Wages in the United States, 1774-Present,

MeasuringWorth, 2014.

5. Samuel

H. Williamson, What Was the U.S. GDP Then? MeasuringWorth,

2014.

6. parliament.uk,

The Financial Revolution, Living Heritage The Glorious Revolution

7. London

Stock Exchange Our History

8. Harvard

Business School, South

sea bubble short history

9.

Hoppit,

J. (2002) The Myths of the South Sea Bubble, Transactions of the Royal Historical Society,

12: 141-165.

10.

Frederic

D. Schwarz, 1772: two

Hundred And Twenty-five Years Ago, American Heritage, 48(6), October 1997.

11.

Cycles in American History

12.

Wright,

Quincy, A Study of War, 1942; reprint ed. Chicago: University of Chicago Press,

1965, p 230.

13.

Ibid

p 1272

14.

Richard

Cavendish, Spanish Bankruptcy, History Today

15.

Spain then and

now;

16th C Spain. Overview: Politics.

16.

Kennedy,

Paul, The Rise and Fall of the Great Powers, New York:

Vintage Book, 1987, p xxiv.

17.

Mitchell,

B. R. British Historical Statistics,

Cambridge University Press, 1988.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}